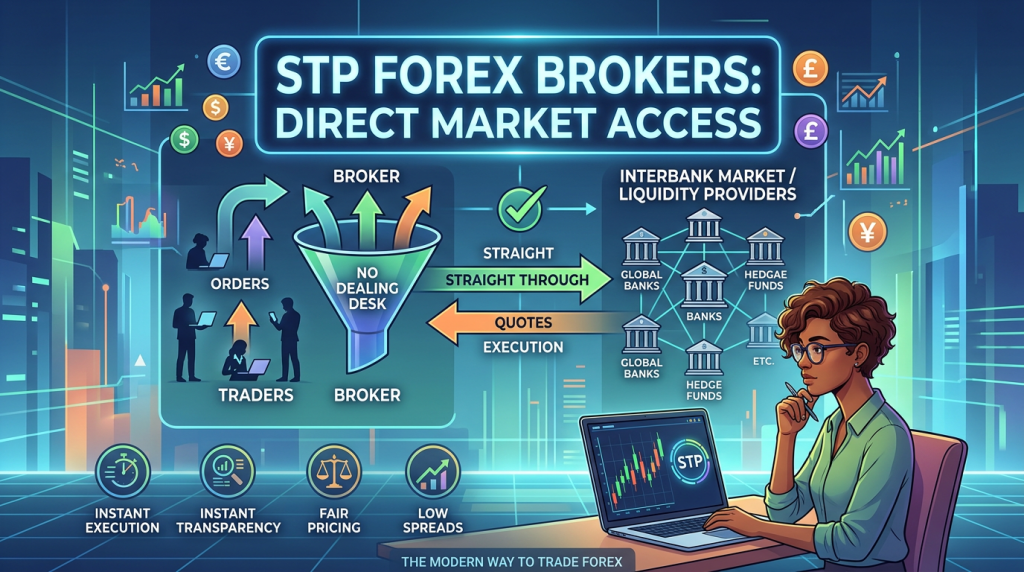

STP forex brokers route client orders straight through to outside liquidity providers with minimal manual dealing. STP stands for straight through processing. The idea is simple enough. You trade against prices that come from banks and non bank dealers, not mainly from a broker’s own dealing desk, and your tickets are hedged outside rather than kept as a big in house bet against you.

Retail marketing turned STP into a badge, often glued on right next to “no dealing desk”. Behind the slogan sits a real structural question. When you buy one lot of EURUSD, who stands on the other side, who hedges what, and how does the broker earn money from that whole chain.

Compared with pure market makers, an STP broker tries to act more like a router than a casino. It earns mainly from spread mark ups and sometimes commission on flow passed into the interbank pool. Compared with a full ECN, an STP broker usually gives you less direct access to the shared order book but still uses outside prices and counterparties.

For traders with some experience, this matters less as an abstract label and more as day to day behavior. It shapes spreads, slippage, how quotes behave when things get busy, and how likely the firm is to view a profitable client as a problem rather than as a source of stable volume.

This article will focus on how STP brokers work and how they compare to other types of forex brokers. If you are looking for a broker to open an account with then I recommend you go to Broker Listings instead. BrokerListings.com is a website designed to make it easy to find and compare brokers against each other.

How STP routing works in practice

Price feeds and aggregation

An STP broker connects to several liquidity providers. These can be banks, non bank dealers, larger brokers or prime of prime firms. Each provider streams two way prices for the forex pairs the broker supports. Those streams arrive as a flow of bids and offers with size attached.

The broker runs an aggregation engine on top of that. For each pair, it compares the best bids across all providers and picks the highest. It does the same for offers and picks the lowest. That gives a composite spread. In some cases the broker also builds a depth ladder, keeping track of how much size is available at the next price levels on each side.

What you see on the trading platform is usually this aggregated top of book with the broker’s own mark up layered on. On some accounts that mark up is zero or very small and you pay a separate commission. On others the commission is folded into the spread. Either way, the price source is an aggregated feed not a single internal quote.

This feed is dynamic. When providers pull back quotes around news, spreads widen on your screen as well. When liquidity is plentiful, they narrow. That is a key difference to a fixed spread market maker that tries to smooth all of that for the client.

Order flow, tickets and hedging

When you send an order to an STP broker, the back end checks which provider is currently quoting the best price that can fill your requested size. It then routes the ticket to that provider, or splits it across several if no single quote can handle everything at a good level. The trade that appears in your account is mirrored by a hedge trade at the provider.

This can be done on a ticket by ticket basis or at net book level. Some brokers choose to offset every trade immediately in matching size. Others internalise tiny trades and only hedge the net exposure once client flow creates a net position in one direction. As long as those net trades go to real liquidity providers, the broker is still operating in an STP way, but with some additional optimisation.

Revenue for the broker comes from the difference between what the provider quotes and what you see, plus any explicit commission charge. STP brokers want as much stable flow as possible through that pipe. They do not need client losses to be large, they need trades to be frequent and the mark up to be wide enough to cover costs.

In an ideal case, this handling is almost invisible for you. You get fills close to the displayed price, positive and negative slippage are both possible, and rejections are rare outside of very busy conditions.

How STP brokers differ from classic market makers

Pricing and execution behaviour

A classic retail market maker generates its own prices. It still takes bank feeds and other reference sources, but a pricing engine inside the firm controls the final bid and ask that reach the client platform. That engine can smooth spikes, widen or tighten spreads and sometimes even skew quotes when flow becomes very one sided.

Because the broker itself stands on the other side of your position, your trades have a direct impact on its risk book. If many clients are long a given pair, the desk is short and needs to decide how much to hedge externally. If client flow is mixed and more or less balanced, it can keep a lot of that risk internal.

This shapes behaviour. Market makers are very comfortable with small, random retail flow that statistically loses money over time. They can quote tight spreads, run promotions and still expect to make good money from spread plus the net result of that noisy client book.

Where they start to feel uncomfortable is with flow that wins often, trades around news, or tries to exploit delayed feeds. A pure market maker can react by widening spreads, rejecting trades during fast moves, adding “last look” checks before fills or even changing account terms for certain clients. All of that is easier to do because the firm controls both sides of the quote.

An STP broker, at least in the clean version of the model, does not run a large internal risk book for most clients. It cares more about keeping the feed honest, spreads realistic and routing fast, since its income is tied more to activity than to the PnL of any one client. It can still adjust mark ups and risk limits, but the direct incentive to shade execution against sharp traders is weaker.

Conflicts of interest and business model

Retail traders talk about “trading against the broker” for a reason. At a market maker you often are. When you lose on a B book account, the broker wins, after costs. That does not mean the firm is out to get you in some cartoon villain sense, but it does mean your losses are part of their revenue line.

That conflict of interest does not exist in the same direct form at a well run STP broker. The firm earns from spreads and commission on orders passed through. It may still internalise some flows, but the business logic is less “how do we extract money from this client book” and more “how do we keep volume coming and spreads tight enough to retain clients but wide enough to cover provider and tech costs”.

There are still conflicts. The broker may get better economics from one liquidity provider than from another and so route flow in a way that is not absolutely ideal for every ticket. It may prefer certain types of client behaviour that are nice and smooth for its hedging. But in comparison with a pure market maker, the tension between client profit and broker profit is smaller.

For a trader you can think of it that way. At a dealing desk, your trading edge has to overcome both market difficulty and the fact that the house is happy when you lose. At an STP broker, you still need to beat the market and pay spreads and commission, but the firm does not directly depend on your failure for its own survival.

STP versus ECN brokers

Matching engines and access to the book

The big difference between STP and ECN is where your order meets other orders. An ECN is a central electronic book. All participants see the same top of book. Large ones see depth as well. Orders from banks, funds and sometimes from the broker’s own clients rest in that book. Matching happens inside the ECN.

An STP broker usually does not plug you into that shared book directly. Instead it receives quotes that already reflect what is happening in the ECNs and single dealer platforms, wraps them into its own stream and sends your orders to whichever provider looks best at that moment. From your seat you are dealing with the broker, not with the ECN.

That may sound like a fine detail, but it affects a few things. With a genuine ECN account that exposes depth, you can see how much size is sitting at each price and even join the book with your own resting orders. On an STP feed, you might see only the best bid and ask, so you have less transparency.

The trade off is that ECN venues often require larger minimum sizes and direct credit lines that retail traders do not have. STP brokers are a middle layer. They give clients quotes shaped by ECN and bank flows but handle the logistics and credit arrangements. That is why many retail accounts that call themselves “ECN” are still technically STP on the back end.

Cost structure and minimum size

Both ECN and STP accounts tend to use raw or near raw spreads plus commission. The difference is that ECN commission is usually tightly linked to actual venue fees and rebates, while STP mark ups can be a bit more flexible. An STP broker might adjust mark up by client group or product, offering tighter spreads on popular pairs, wider ones on exotics.

Minimum trade size is another area where ECN and STP diverge. True ECN venues expect reasonably chunky orders. Retail ECN style accounts work around that by aggregating client flow. An STP broker can accept micro lots from clients and then bundle them into bigger hedges with its providers.

For you this means that an STP broker can be friendlier for small account sizes than a hard line ECN environment. You get some of the benefits of ECN pricing without being forced into larger tickets than you want. The cost per trade is still largely transparent, since spreads and commission can be measured, but you do not need institutional size to play.

On the other hand, if you are a high volume, low latency trader, a true ECN with direct access might shave just enough off costs and slippage to matter. In that case STP can feel like an extra hop that you would rather avoid. For most retail traders though, that is not the bottleneck.

Hybrid models, A book and B book mixes

Why most “STP only” stories are not fully true

In marketing, brokers like clean labels. STP only. ECN only. No dealing desk. The real world is more mixed. Most retail forex brokers operate hybrid books. They route some flow to outside providers and keep some in house. Those pools are often called A book for hedged flow and B book for internalised flow.

Small, noisy accounts that follow typical losing patterns are cheap to internalise. Hedging every tiny trade externally would increase fees and complexity for no real benefit. So many brokers push those accounts into the B pool. Size is easy to manage, spreads and payouts can be adjusted, and the net result tends to be a slow gain for the firm after costs.

Flow that is larger, more aggressive, or consistently profitable is harder to warehouse. Brokers defend themselves by sending that flow straight to their liquidity providers, sometimes through an ECN hub. That is the A pool. In that zone, the broker behaves more like a classic STP shop.

So a client base inside the same broker can be split. Two traders on “STP accounts” may experience slightly different execution behaviour because their flow gets routed differently. From a pure brand view the broker can still claim to be STP. From a technical view, it is doing a mix of internalisation and pass through.

What this means for an individual trader

For a retail trader, this hybrid reality is almost certain. The question is not “does my broker ever internalise” but “how do they behave when they do, and when do they choose to pass flow through instead”.

If you trade small size, avoid news, hold trades for a while and do not push fancy latency games, you will probably not trigger much special treatment. A decent broker can happily route your orders through its normal pipes without worrying. Whether that is pure STP or some mix matters less than the end results you see.

If you trade in ways that stress a broker, such as news scalp strategies, arbitrage across feeds or very aggressive short term trading, routing decisions become more sensitive. Some firms will push you to A book quickly, which is what you want if your edge is real. Others will try to limit or discourage your activity.

The practical response is simple. Watch fills. Track slippage. Pay attention to how spreads and execution behave when you increase size or change style. The label on the account page matters a lot less than whether the platform still treats you fairly once there is real money at stake.

STP versus DMA and prime style access

Where STP sits on the access ladder

Direct market access in forex usually talks about a client’s ability to send orders straight into a bank or ECN book with very little broker intervention. At the top end, funds with prime broker relationships plug into matching engines with their own IDs. That is as close as you get to “raw”.

STP sits a couple of rungs below that. You still rely on the broker to aggregate feeds, manage credit to providers and handle net hedging. You do not hold your own prime account. For most individual traders that is fine, because the cost and legal work involved in full DMA access is huge.

In a sense, STP is retail DMA. You are not stuck dealing only against the house. You are not expected to post millions as collateral at a bank. You are sharing the broker’s pipes, and getting a cleaned up version of what sits on the other side.

How larger players use similar plumbing

The funny part is that even many larger players use something that looks like STP, just with more zeros. Prime of prime brokers aggregate prices from tier one banks and ECNs, then offer that composite feed and routing service to smaller banks, brokers and funds. Those downstream clients are doing with their clients exactly what your STP broker does with you.

So STP is not a poor cousin. It is the same pattern seen all along the chain: someone sits between end users and the main liquidity pool, managing credit, technology and aggregation. The difference is scale and how much direct control each layer has over risk.

Which trader profiles fit STP brokers best

Short term traders

Short term traders care about execution more than most. They might trade off five minute charts or even shorter, enter several times per session and lean on tight stops and modest targets. For them, spread, slippage and trade acceptance are a big chunk of the game.

An STP broker with decent providers is usually a better fit than a pure market maker here. Variable spreads that mirror real liquidity help you avoid trading during thin patches. Commission based pricing lets you see your cost per trade clearly. If slippage is reasonably fair in both directions, you can plan around it.

True ECN access can be even better if your size justifies it and your method uses resting orders as well as market orders. But many retail traders run size and capital levels that are still better served through a broker who handles all the machinery in the background. For them, a good STP broker is a practical sweet spot.

Swing and position traders

Swing traders and position traders open fewer trades and hold them longer. They watch the daily chart, maybe the four hour, and let positions run over days or weeks. For them, pip level differences in spread or odd half pip of slippage here and there matter less than other factors.

What matters more is honest swap charging, sensible margin policy, stability around rollovers and corporate action handling if they trade CFDs as well as spot. On those fronts, an STP broker is neither automatically better nor worse than a solid market maker. It comes down to that firm’s operations and regulatory home.

Some swing traders still prefer STP because they like the idea that their positions are hedged outside and that their profit is not a direct line item against the broker’s PnL. Others are happy at a dealing desk that has treated them well and offers built in risk tools. For this group, broker type is just one item among many, not the top one.

How to judge whether an STP broker really behaves like one

Marketing copy will not give you the full answer, so you have to combine what the broker says with what you can observe.

The first check is the fee and spread grid. A genuine STP model usually shows variable spreads and either a clear mark up or an explicit commission. Headline fixed spreads with no mention of pass through costs are more typical of a pure dealing desk.

The second check is transparency about liquidity providers. Some brokers name banks and prime partners in their documents. That is not proof of perfect routing, but it beats vague talk about “tier one liquidity” with no names at all.

The third check is your own trade history. Over a few hundred trades, look at how often you get positive slippage and how often negative, and by how much. Watch spreads around scheduled news. See whether order rejection rates spike in ways that do not match what you see on independent price feeds.

Regulation and history still matter. An STP label on a firm under a strong regulator with a clean record is a different thing than the same label on an offshore entity with no meaningful oversight. Even with STP routing, you are leaving money with a company and trusting its internal controls.

In the end, STP is one piece of the puzzle. It tells you that the broker at least intends to pass your trades into the wider forex pool instead of keeping them all in a back room book. How well it does that, and whether that fits your own style and risk tolerance, comes down to details you can only see by looking past the slogan and watching how the account behaves when money and stress are real.

This article was last updated on: March 5, 2026